¿What is High Frequency Trading?

[dropcap]High[/dropcap] Frequency trading involves the use of algorithms to buy and sell in microseconds (one million seconds), milliseconds (one thousand seconds) through thousands of trades.

If you want to learn a little bit more you can read the previous link. The objective of this article is more legal and focused on the regulations and the current situation of this particular form of possible «manipulation of the financial markets».

To give you an idea while normal traders do a single trade, they make thousands and get a benefit to the market, High frequency traders make thousands and get an advantage in the market. Technically speaking can imply a competitive advantage for them in case the regulator don´ t watch them. Moreover, as is usually the case, society lags behind regulating the complexities of the market.

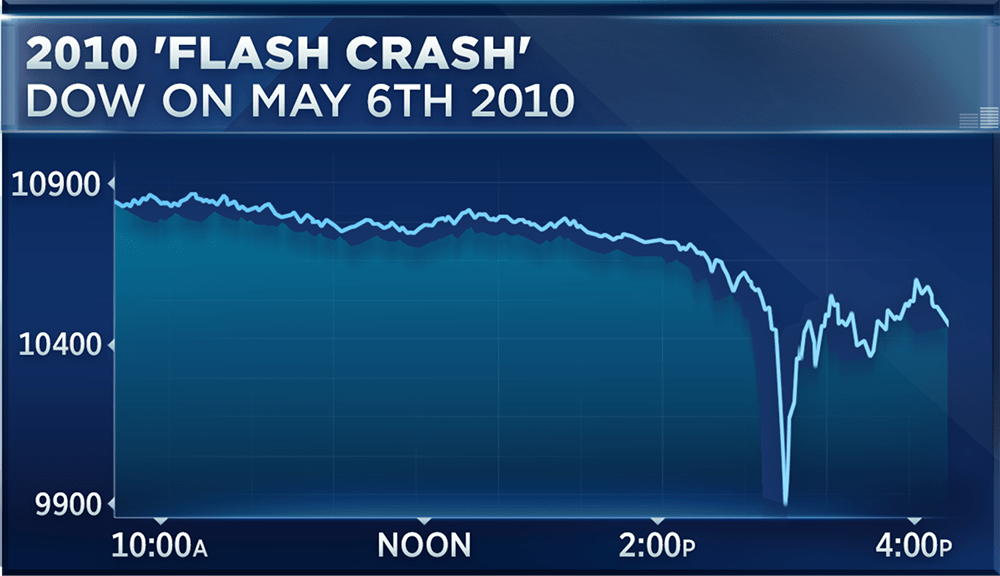

It is important that you understand that this can affect all of us all because it can cause chaos, just ask Navinder Singh Sarao who was responsible for the Flash Crash on May 6, 2010 Flash Crash del 6 de mayo de 2010.

Another disastrous example was the 1000 point fall in the Dow Jones Industrial Average on August 25, 2015 that must also be remembered in order to avoid a repeat …

High frequency Trading is increasing every year according to the report of the Research Service of the United States Congress (hereinafter Re-US). According to this report, High Frequency Trading comprises 55 % US stock market and 40 % in Europe.

There are two ways to place the order in the market:

First- Through a direct access (Direct Market Acces). The trade activities go directly to the market without going through a Broker. In short, the broker gives them the key to direct access to the market, which favors greater privacy in transactions and less commissions to pay.

Second- Sponsored Access. It is when another entity allows you access to the market.

If you want see this documentary and you will learn the basics about high frequency trading:

The Law in High Frequency Trading

Before going on to explain the different legal bodies in Europe and the United States, the first thing to understand a possible competitive advantage is knowing the 2 types of strategy the algorithm uses:

a) Creation of a market that involves obtaining a profit thanks to the margins between supply and demand.

b) Take advantage of margins/price differences (arbitrage) between different platforms.

Yes, it is a little abstract, but Let me explain it in a simple way. In the first case if A sells at 5 and B buys at 2, what a high frequency trading program would do is buy at a price between 5 and 2 at a vertigo speed to get rid of the position as soon as possible, earning small amounts with thousands and thousands of trades. Regarding arbitration, it is similar but with different platforms. The algorithm buys an asset on a platform at a price and sells it – the same asset – at a better price on a different platform. As there are different platforms, their prices have differences that are exploited by the algorithms for their own benefit.

Legal definition of HFT according to the European Parliament

«High Frequency Trading means trading in financial instruments where a computer algorithm automatically determines individual parameters of orders such as whether to initiate the order, the timing, price or quantity of the order or how to manage the order after its submission, with limited or no human intervention, and does not include any system that is only used for the purpose of routing orders to one or more trading venues or for the processing of orders involving no determination of any trading parameters or for the confirmation of orders or the post-trade processing of executed transactions”. ”

Characteristics of high frequency trades:

1. It uses facilities of shared location, direct access to the market or proximity accommodation;

2.- Involves a daily trading volume of at least 50%;

the percentage of canceled orders (including partial cancellations) is greater than 20%; most positions close on the same day; more than 50% of the orders or trades carried out in trading centers that offer discounts or reductions in relation to the orders that offer liquidity are eligible for said reductions «.

Europe High Frequency Trading Regulation

1º) First of all Directive 2004/39/EC of the European Parliament and of the Council of 21 April 2004 on markets in financial instruments amending Council Directives 85/611/EEC and 93/6/EEC and Directive 2000/12/EC of the European Parliament and of the Council and repealing Council Directive 93/22/EEC it left out the High Frequency Operators (HFT) according to its article 2.1.d). This article says that this law does not apply to «persons who do not perform services or investment activity on their own account». Taking into account that many of these organizations do it on their own they seem to have found a way to avoid the application of this directive.

Fortunately, Directive 2004/39 / EC on the markets for financial instruments completes these gaps. You can see a summary in Markets of financial instruments (MiFID) and investment services.

2º) DIRECTIVE 2014/57/EU OF THE EUROPEAN PARLIAMENT AND OF THE COUNCIL of 16 April 2014 on criminal sanctions for market abuse (market abuse directive) came to surpass these lack of regulation in its

Article 5

Market manipulation

For the purposes of this Directive, market manipulation shall comprise the following activities:

(a)

entering into a transaction, placing an order to trade or any other behaviour which:

(i)

gives false or misleading signals as to the supply of, demand for, or price of, a financial instrument or a related spot commodity contract; or

(ii)

secures the price of one or several financial instruments or a related spot commodity contract at an abnormal or artificial level;

unless the reasons for so doing of the person who entered into the transactions or issued the orders to trade are legitimate, and those transactions or orders to trade are in conformity with accepted market practices on the trading venue concerned;

Photo by Stephen Dawson on Unsplash

3º) If you consult us from Spain, do not forget the Royal Legislative Decree 4/2015, of October 23, which approves the revised text of the Securities Market Law (see below the existence of the draft amendment) that already includes algorithmic negotiation in its article 139, so our legislation has amended the error that we mentioned earlier regarding the 2004 directive.

It is common sense, and so do the corresponding laws oblige operators to establish mechanisms that identify risks that compromise the trade, as well as a fair and orderly negotiation. I, particularly do not believe in justice in the market, since they are the jungle in the modern version, where some take money away from others, so it is difficult for the regulator to establish technical mechanisms for bringing justice to the market manipulators. Don´´ t have any doubt that they exist…

According to the aforementioned Directives, investment services companies are obliged to communicate the operations of financial instruments to the competent authority before the next day according to the MIDIF directive. Not doing so it´´ s considered Bad practice but to prove it you ll need to recruit experts.

As of the date of this article, the Proposed Draft Law of the Securities Market in Spain is currently in process to redefine «Algorithmic Negotiations» to strengthen controls and reduce operational risks. The preliminary draft does not differ much from what legal community claims in order to gain control over the operations: who perform them and how to prevent anomalies, such as limit the «not executed» orders and slow down the flow of operations in the event of a possible catastrophe. This is a control never seen to date. We will have to see how this is developed in the real arena for the institution to keep track of all those operations. The ESMA (European Securities and Markets Authority), for example, does foresee the creation of a permanent vigilance commission to control manipulation in the market.

4º) Another interesting publication in this topic are the guidelines on systems and controls applied by the platforms. The investment services companies and the competent authorities in an automated negotiation environment that published ESMA, a kind of European Securities Market Commission, which establishes a series more focused on technical aspects such as:

a) Manage the volumes of messages that they receive.

b) Do the due diligence of the applications for admission entities that are not investment services companies

c) Likewise, they must establish controls before and after the operations carried out by their members, participants and users (including filters on the price and volume of orders), being able to cancel, modify or correct an operation, as well as restrict or prevent the hiring financial instruments to maintain the orderly functioning of the market (for example, automatically rejecting orders that exceed certain volume or price thresholds). Likewise, they must implement mechanisms to avoid the excessive inflow of orders at a specific time, imposing limits on the introduction of orders per participant.

c) Requirements to prevent market abuse and its manipulation.

d) Requirements in case of direct or sponsored access.

High Frequency Trading Rules in EE.UU

Europe is behing EE.UU in this matter. In fact it has proven experience in going after many real cases of manipulation as in 2016 with Barclays and Credit Suisse, in October 2014 in the Treasury market, the fine that Coscia and Panther Energy paid for 2.8 million in 2013, a civil action against 3RedTrading, etc.

The main law that regulates this matter in the US is the Dodd Frank Act in conjunction with the Security Exchange Act

In short you can see throughout the article as it is usual for some laws to copy others and also that the laws are behind the reality especially taking into account, and according to wikipedia, that high frequency trading or high frequency operations it has been long, in particular since 1999.

Bibliography:

1º) La denominada negociación automatizada de alta frecuencia

(High Frequency Trading).

Características y regulación.

Miguel Sánchez Monjo y Ana Pineda Martínez

Revista de Derecho del Mercado de Valores nº 12/2013 (enero-junio)

2º) High Frequency Trading:

Overview of Recent Developments del Servicio de Investigación del Congreso de EE.UU

Rena S. Miller

Specialist in Financial Economics

Gary Shorter

Specialist in Financial Economics

April 4, 2016

ESMAS (European Securities and Market Authority). Date: February 24, 2012 ESMA / 2012/122 (ES)

4º) Glossary of simple questions

Deja una respuesta